By using customer identification or “know your customer” rules, banks try to prevent money laundering and other financial frauds. This use of customer identification rules by banks is contemplated at the Fifth Recommendation of the Financial Action Task Force. The Fifth Recommendation urges banks to diligently verify a customer’s identity and to record the true beneficial ownership of bank accounts.

As reported at “Fighting Financial Fraud At UK Banks“, the UK changed its banks’ “know your customer” rules on December 15, 2007, by codifying them at Money Laundering Regulations 2007*. U.S. banks too verify customer identities, but do so pursuant to 31 C.F.R Part 103.121. Lawsuits alleging that two U.S. banks had failed to sufficiently identify their bank customers, are respectively described at: “Associated Bank Sued For Supposedly Ignoring Red Flags” and “Lawsuit Claims Wachovia Bank Facilitated Alleged Ponzi Scheme“.

UBS AG and other Swiss banks also require customer identification at the time a bank account is opened. The customers of Swiss banks execute a declaration of beneficial ownership, commonly referred to as a “Form A”. A July 13, 2001 “Form A” was used in the U.S. tax fraud case brought against Florida yacht broker Robert Moran. According to the Plea Agreement in Mr. Moran’s case, the July 13th “Form A” helped demonstrate that Mr. Moran had violated 26 U.S.C. § 7206 (1), (perjury on a return / false statements).

A comparison between Mr. Moran’s individual tax returns for the years 2001 through 2007 and his “Form A”, revealed that Mr. Moran had maintained secret Swiss bank accounts at UBS AG. These Swiss accounts were kept in the name of the Panamanian corporation Winter Drive Investments S.A. (Page 2, Statement of Facts, attached to Plea Agreement).

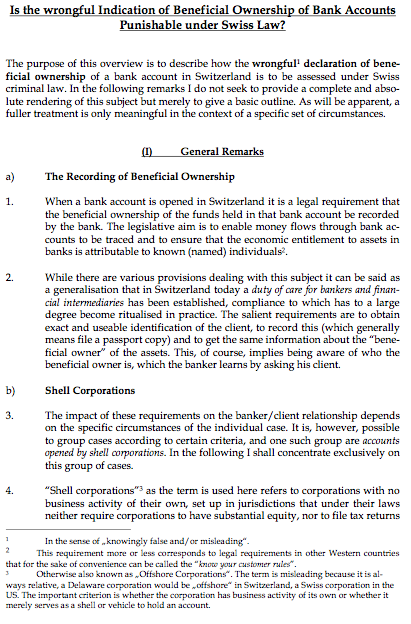

The legal memo reproduced below discusses the required use of “Form A’s” at Swiss banks. It was supplied by Swiss counsel who is a doctor of laws from Zurich University, has practiced in Zurich, New York & Hong Kong and was a visiting scholar at Yale Law School. The legal memo shows how a bank customer falsifying beneficial ownership in a “Form A”, could violate Swiss criminal law:

(To Read The Entire Legal Memo, Click On It Above)

(To Read The Entire Legal Memo, Click On It Above)

Swiss counsel additionally made the following critical comments which relate to the memo and give a glimpse of the current legal climate in Switzerland:

“1) Due in part to the current upheavals concerning the activities of major Swiss banks in the US, the law on financial regulation in Switzerland is somewhat uncertain. Though this is against Swiss legal tradition, the anti-money laundering rules in Switzerland follow what I believe is international practice in deliberately using a degree if vagueness about the exact standards to be applied so as to induce a “chilling effect”. This uncertainty is rendered more acute by the difficulty of assessing the interaction between the laws of various nations.

Note also that the rules and regulations have created a web of disclosures and of duties to investigate. It will be a brave person who in search of fiscal relief will navigate through this web without fear of having to make any misleading or materially wrong declaration (thus doing more than mere non-disclosure).

One practical result of the current problems with the US is that banks and Financial Intermediaries in Switzerland (and elsewhere in Europe) have simply stopped dealing with US nationals or US residents (except possibly through US based “on shore subsidiaries” of foreign banks), to the extent of closing long standing business relationships even in the absence of any specific allegation of wrongdoing, fiscal or otherwise. Thus while the law may not have changed, the climate in which the law operates has.

2) In step with this development, the required standard of care expected of a Financial Intermediary (including a bank) is much higher and increasing continuously. Today quite sophisticated profiling and automatic monitoring of all transactions is routine. The effect of this is the same as mentioned above, the law has not fundamentally changed but the loopholes have become very small in practice. Mere “non disclosure” is only effective if nobody asks. Note also that current practice requires on-ongoing checks, not merely checks at the opening of the account bur also during its operation. ”

*Money Laundering Regulations 2007, is reproduced under the terms of Crown Copyright Policy Guidance issued by HMSO.

Copyright 2010 Fred L. Abrams